The November edition of the Global VAT Guide features comprehensive updates on many VAT regulations and developments across Europe, Asia the Middle East and the Americas from Belgium, Croatia, France, Hungary, Ireland, Italy, Latvia, Portugal, Romania, Slovenia, Sweden, Bhutan, Columbia, Kazakhstan, Switzerland, UAE and the United Kingdom.

Use this summary to stay informed of the latest regulatory changes, effective dates and compliance implications for your business.

Belgium

Postponement of VAT chain legislative package

Published: 26 August 2025 | Effective: 1 October 2025

Summary:

The Federal Public Service Finance (FPSF) has indefinitely postponed the implementation of the VAT Chain legislative package, originally scheduled for 1 October 2025. The delay allows taxpayers, accountants and tax advisors to better prepare for the upcoming eInvoicing rollout in 2026 and ensures a smoother transition to digital VAT reporting.

On 26 August 2025,the Federal Public Service Finance (FPSF) posted an update in relation to the VAT chain legislative package for taxpayers. The VAT chain is aimed at modernising tax collection in Belgium. This announcement has been officially enacted through Circular 2025/C/62, effective 1 October 2025.

Following consultations with the Institute for Tax Advisors and Accountants (ITAA), the FPSF have decided to postpone the implementation of the VAT Chain package indefinitely to ensure a smooth transition for all reporting taxpayers.

The postponement aligns with the upcoming introduction of eInvoicing in Belgium in 2026, which will significantly transform the digital VAT reporting landscape. By allowing additional preparation time, both tax advisors and accountants will be better equipped to adapt to digital invoicing processes and related challenges. This delay also provides an opportunity to refine the VAT Chain system based on real-world feedback, ensuring a more comprehensive and taxpayer-friendly implementation.

The ITAA and FPSF continue to collaborate on establishing a realistic and gradual timeline, supported by concrete guidance and documentation. Additionally, taxpayers should note that the bank account for VAT payments will remain unchanged after 1 October 2025 – BE22 6792 0030 0047.

The filing deadlines also remain the same:

- Monthly filers: by the 20th of the month following the tax period

- Quarterly filers: by the 25th of the month following the tax period

(Deadlines are extended to the next working day if they fall on a weekend or public holiday.)

Corrective VAT declaration schemes, penalties outlined in the original draft law and the VAT refund request process will not take effect until further notice.

Croatia

Draft VAT Act amendments proposed for 2026

Published: 18 October 2025 | Effective: Planned for 1 January 2026

Summary:

The Croatian Ministry of Finance has proposed amendments to the VAT Act aimed at simplifying administrative processes and adjusting filing deadlines for VAT taxpayers. These changes are part of broader efforts to align VAT procedures with the upcoming mandatory eInvoicing system.

If adopted, the amendment will introduce several key administrative simplifications and deadline adjustments for VAT taxpayers.

Extension of filing deadlines

- Current rule: VAT returns and related reporting forms are due by the 20th day of the month following the respective tax period.

- Proposed rule: Deadline extended to the last day of the month following the respective tax period.

Administrative simplifications

- eInvoicing: Recipient consent is not required for eInvoices where mandatory under fiscalisation rules

- Elimination of redundant reporting forms, whose content will be incorporated into eInvoicing data, including:

- Form DON-H: Reporting of food donations

- Form I-RA: Sales Ledger (paper or electronic)

- Form U-RA: Purchase Ledger

- VAT-F Form: Special records on goods sold to customers in passenger traffic

- Form PPO: Application for domestic deliveries subject to reverse charge

The public consultation on the draft bill concluded on 18 October 2025, and the proposal is now awaiting parliamentary approval.

France

Phased rollout of eInvoicing and eReporting begins

Published: October 2025 | Effective Starting 1 September 2026 (Phased implementation)

Summary:

The French tax authorities have issued detailed guidance on mandatory eInvoicing and eReporting obligations, including phased implementation timelines, transaction scope, and reporting requirements. The rollout is structured by enterprise size and VAT registration status.

- Implementation timelines

- Large enterprises: Annual turnover above €1.5 billion. Required to issue eInvoices and submit eReporting data from 1 September 2026.

- Medium enterprises: Annual turnover above €50 million. Required to issue eInvoices and submit eReporting data from 1 September 2026.

- Small and micro enterprises: Must be able to receive eInvoices from 1 September 2026. They will be required to issue eInvoices and submit eReporting data from 1 September 2027.

- Non-established businesses: Exempt from eInvoicing, but must fulfil eReporting obligations starting 1 September 2027.

From 1 September 2026, all French establishments must be able to receive eInvoices.

eInvoicing

- Scope of eInvoicing

- eInvoicing applies to:

- B2B transactions between French VAT-registered companies

- B2C and cross-border transactions are out of scope of eInvoicing and fall under eReporting

- eInvoicing applies to:

eReporting

- eReporting covers the following:

- B2C transactions (sales to end customers)

- Cross border transactions including:

- Intra-EU supplies and acquisitions of goods and services,

- Exports to non-EU entities

- Activities in overseas territories

- Transactions by non-established companies

- eReporting data requirements are:

- Customer identification (name, SIREN number, and address)

- Invoice number and date

- Description of goods or services supplied

- Gross amount, VAT amount, and VAT rate

- Payment date

- eReporting frequency and deadlines:

Reporting frequency varies by VAT regime: monthly, quarterly, or simplified. Reporting Frequency and Deadlines are:

- Monthly VAT filers:

- Transactions from 1–10 of the month → due by 20th of the same month

- Transactions from 11–20 → due by 30th of the same month (except February)

- Transactions from 21–end of the month → due by 10th of the following month

- Quarterly VAT filers:

- Must report monthly, by the 10th of the following month

- Simplified VAT regime filers:

- Must report monthly, between the 25th and 30th of the following month.

Actions for businesses:

- Confirm readiness to receive and issue eInvoices according to enterprise size.

- Review internal systems and reporting workflows for eReporting obligations.

- rain accounting and compliance teams on phased deadlines and submission procedures.

- Monitor updates from French tax authorities for official guidance on data format and technical specifications.

France

VAT exemption threshold reinstated

Published: 23 October 2025 | Effective: Retroactive from 1 March 2025

Summary:

Following strong opposition from small businesses, the French Government has abandoned plans to introduce a unified VAT exemption threshold.

Key changes:

Under Bill No. 6 of 23 October 2025, the previously applied differentiated thresholds for goods, services and certain professional activities have been reinstated.

The proposed €25,000 unified threshold and its €27,500 tolerance margin are no longer applicable.

Impact:

- Small businesses must continue to apply existing differentiated VAT exemption thresholds.

- Retroactive effect from 1 March 2025 ensures continuity of compliance and prevents unintended non-compliance under the abandoned unified threshold.

Hungary

Switch from paper-based receipts to e-cash registers

Published: July 2025 | Effective:1 July 2025 (transition period until 1 September 2026)

Summary:

Hungary has modernised its tax reporting system, eliminating the requirement for businesses to submit data from manual receipts. This marks a significant step in improving compliance, transparency, and administrative efficiency.

Key changes:

- Mandatory reporting: Businesses must transition to the new receipt data reporting framework by 1 September 2026.

- Scope: Approximately 270,000 businesses will be affected.

- E-cash registers: Adoption is voluntary until September 2026 but recommended for simplified compliance.

- Real-time data reporting: Already covers invoices, online cash registers, and vending machines; will extend to paper receipts through risk-based monitoring.

Impact:

- Reduces administrative burden for businesses by eliminating manual receipt reporting.

- Enhances transparency and visibility into business income for the National Tax and Customs Administration (NAV).

- Supports Hungary’s broader economic objectives, including combating tax evasion.

Ireland

Replacement of ROS Offline with Return Preparation Facility (RPF) for Intrastat filings

Published: September 2025 | Effective: 1 January 2026

Summary:

The Irish Revenue Online Service (ROS) has introduced the Return Preparation Facility (RPF) web application to replace the ROS Offline tool for Intrastat filings. From 1 January 2026, filings via ROS Offline will no longer be accepted.

Key changes:

- Mandatory RPF usage: All Intrastat filings must be submitted via RPF. ROS Offline will cease to be maintained for Intrastat purposes.

- CSV templates: Templates are hardcoded for RPF and must not be modified.

- File submission: Completed forms in RPF generate a structured file to upload directly to the ROS platform for periodic reporting.

- Form integration: New forms are continuously added to RPF (e.g. VAT3 integrated in March 2025). Some forms remain in ROS Offline but will be migrated in the future.

Technical and operational details:

- Supported browsers: Microsoft Edge, Google Chrome, Opera

- RPF is accessible even during ROS scheduled maintenance.

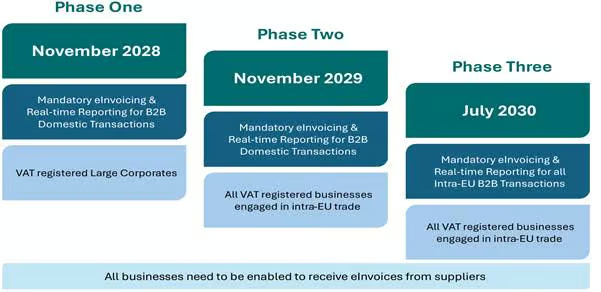

Ireland

Real-Time Reporting & eInvoicing Rollout

Published: 8th October 2025 | Effective: Phased rollout from November 2028

Summary:

Irish Tax and Customs has published a timeline for eInvoicing and Real-Time Reporting (RTR) as part of the VAT Modernisation Project, aligned with the VAT in the Digital Age (ViDA) initiative by the European Commission. The phased rollout is designed to reduce compliance burdens and modernise VAT reporting across all taxpayer categories.

Implementation timeline

Phased digitalisation plan aligned with ViDA

- November 2028: All businesses must be able to receive eInvoices

- November 2029: Large corporates and VAT-registered traders engaged in intra-Community B2B trade must implement RTR and eInvoicing for domestic B2B transactions

- July 2030: RTR and eInvoicing extend to both domestic and intra-Community B2B transactions for all VAT-registered taxpayers involved in intra-EU trade

Scope and objectives

- B2B domestic transactions: Initially targeted for large corporate entities, then extended to all VAT-registered taxpayers involved in intra-Community trade.

- Intra-Community B2B transactions: Included from July 2030 onward.

Key objectives:

- Reduce administrative and compliance burdens.

- Ensure timely, accurate VAT reporting.

- Support the broader ViDA project and European digital VAT strategy.

Implementation Approach

- Practicality and flexibility: Rollout designed to accommodate businesses of all sizes.

- Stakeholder collaboration: Irish Tax and Customs are coordinating with tax practitioners, software providers and industry representatives.

- Technical robustness: Systems will be tested and supported to ensure a smooth transition to digital VAT reporting.

Impact:

- Businesses will need to adopt eInvoicing and RTR systems progressively over a multi-year timeline.

- Enhances transparency, efficiency and compliance across domestic and intra-Community VAT reporting.

- Requires coordination between finance teams, IT systems, and external software providers.

Actions for businesses:

- Begin planning for phased adoption of eInvoicing and RTR.

- Review IT and accounting infrastructure for compatibility with upcoming digital VAT systems.

- Engage with software providers and tax advisors to ensure compliance with rollout deadlines.

Italy

VAT recovery for the 2026 Olympic Winter Games

Published: October 2025

Relevant for expenses incurred during:

- Olympic Winter Games: 6–22 February 2026

- Paralympic Winter Games: 6–15 March 2026

Summary:

The 2026 Olympic Winter Games will generate significant business-related expenses for companies operating in Italy, including broadcasters, media agencies and service providers. These expenses, such as accommodation, transport, catering, and event-related services, may be subject to Italian VAT, which can be recovered under specific conditions.

VAT recovery for EU-based companies

- EU-established companies can reclaim Italian VAT under Directive 2008/9/EC.

- Procedure: Submit an electronic refund request via the VAT Refund e-Portal of the home country’s tax authority, which forwards the request to the Italian tax authorities.

- Scope: Eligible business-related expenses only; certain costs (e.g. private travel or entertainment) may be restricted.

VAT Recovery for Non-EU Companies from Reciprocity Countries

- Countries with reciprocity agreements include Israel, Norway, Switzerland, and the United Kingdom.

- Procedure: Refund claims submitted by post to the Italian Tax Office responsible for foreign VAT refunds.

- Eligibility: Qualifying business expenses incurred in relation to the Games.

VAT recovery for non-EU companies from non-reciprocity countries

- Companies from countries without reciprocity agreements (e.g. Australia, China, Brazil, India, United States) can recover VAT by following local procedures, which include:

- Appointing a fiscal representative in Italy and registering for VAT before incurring expenses.

- Complying with Italian VAT obligations, including periodic and annual returns and maintaining invoices.

- Submitting a VAT refund claim via the applicable Italian procedure.

Special requirements:

- Refunds exceeding €30,000 require a bank guarantee equal to the refund amount plus applicable interest, valid for three years.

- Guarantee may be waived if the refund is certified by a registered accountant with required supporting documentation.

Impact:

Enables businesses from any country to recover Italian VAT but requires careful planning, resource allocation, and strict compliance with Italian VAT rules.

Potential future extensions of reciprocity

Discussions are ongoing regarding expansion of Italy’s reciprocity list, potentially accelerated by the 2026 Olympic Games. Possible future inclusions:

- Countries without VAT or a similar system (e.g. Hong Kong, Kuwait, Qatar)

- Countries offering reciprocal VAT refunds to Italian businesses (e.g. Australia, Canada, Japan, Iceland, New Zealand)

- Jurisdictions with different indirect tax systems (e.g. United States)

Note: These changes are hypothetical and may only materialise in the long term.

Latvia

B2B eInvoicing implementation

Published: 5 July 2025 | Effective: 1 January 2028 (mandatory), voluntary from 1 January 2026

Summary:

The Latvian Parliament has postponed the mandatory B2B eInvoicing requirement from 1 January 2026 to 1 January 2028, following stakeholder feedback. The phased approach is intended to support small and medium-sized businesses in implementing digital tools, ensuring compliance, and establishing reliable e-communication channels.

Mandatory eInvoicing for transactions with public sector entities has been in effect since 1 January 2025.

Scope and Applicability

- Entities covered: All VAT-registered taxpayers, domestic or foreign, are classified as “commercial companies” and must comply.

- Foreign companies holding a Latvian VAT registration number will be required to issue eInvoices for domestic transactions from 1 January 2028.

- Public sector transactions: Already mandatory since 2025; invoices must be submitted electronically via VID platforms.

Supported eInvoicing Formats

- PEPPOL BIS Billing 3.0

- LVS EN 16931-1+A1+AC

- Both formats are XML-based.

- VID tools: eAddress platform, supporting documentation, sample files, and schema references are provided to facilitate compliance.

- All eInvoices must be transmitted to VID to be recognised as legally valid.

Timelines and phased rollout

- Voluntary B2B adoption: (1 January 2026) Businesses may begin issuing eInvoices through official and private platforms.

- eAddress platform availability (30 March 2026) Official platform open for voluntary B2B eInvoicing reporting.

- Mandatory B2B eInvoicing (1 January 2028) All VAT-registered businesses must issue eInvoices for domestic transactions.

Objective

- Allow both state platforms and private service providers to test, refine and stabilise their systems ahead of the 2028 mandate.

- Ensure a smooth transition for businesses to fully digital reporting.

Additional Considerations

- Continuous Transaction Control (CTC): No CTC model has been legislated; technical and procedural details are still being refined.

- B2C transactions: Currently exempt from eInvoicing requirements.

- Pre-filled tax returns: Not yet introduced or discussed based on eInvoices validated by VID.

Impact:

- Provides small and medium-sized businesses additional time to implement eInvoicing systems.

- Establishes a clear roadmap for gradual adoption and legal compliance.

- Enhances digital reporting capabilities while ensuring system stability ahead of the 2028 mandate.

Portugal

Extension for PDF invoices considered as eInvoices

Published: 9 October 2025 | Parliamentary Process: October–November 2025

Summary:

The draft State Budget for 2026 (Lei n.º 37/XVII/1.ª) was published on 9 October 2025. Among the proposed measures is the extension of the provision allowing PDF files to be considered electronic invoices for all purposes under tax legislation (Chapter V, Article 80) until 31 December 2026. This publication initiates the parliamentary budget procedure, which will progress through multiple stages and conclude with a final vote scheduled for 27 November 2025.

The draft budget is now progressing through the parliamentary procedure, which includes debates, committee hearings and votes, culminating in the final vote scheduled for 27 November 2025.

Key stages of the Parliamentary Calendar

- 27–28 October: Debate and vote on the general principles of the State Budget for 2026

- 29–31 October: Committee hearings on the State Budget

- 3–7 November: Continuation of hearings

- 20–21 November: Debate and vote on specific provisions

- 24, 26–27 November: Detailed debate and final overall vote

Key Provision: PDF Invoices

- Scope: All PDF files issued as invoices may continue to be recognised as electronic invoices under Portuguese tax law.

- Effective until: 31 December 2026 (pending parliamentary approval).

- Implication: Provides businesses with continued flexibility in electronic invoicing while legislative updates are assessed.

Portugal

VAT Group

Published: 20 October 2025 | Effective: Pending further guidance

Summary:

The Portuguese National Assembly has formally introduced VAT Groups into Portuguese tax law, aligning the country with practices in other EU Member States. The reform allows closely related entities to consolidate VAT reporting under a single group structure, while maintaining compliance obligations at the individual entity level.

Structure and eligibility

- Dominant (parent) entity:

- Must hold at least 75% of the share capital of each subsidiary.

- Must possess more than 50% of voting rights in the subsidiaries.

- Subordinate entities:

- Must participate in a shared or common economic activity.

- Must be established in Portugal, or if established in the EU/EEA, meet equivalent administrative and tax obligations.

Reporting and compliance

- Centralised VAT compliance:

- The dominant entity is responsible for consolidated reporting and payment for all group members.

- Consolidated VAT return: Due by the 10th of the second month following the tax period.

- Consolidated VAT payment: Due by the 15th of the same month.

- If deadlines fall on a weekend or national holiday, they shift to the next working day.

- Individual entity obligations:

- Each entity must continue submitting its own VAT return.

- Individual VAT liabilities remain payable separately.

Outstanding guidance

The Portuguese Tax Authority has yet to issue detailed instructions on:

- Application of SAF-T (Standard Audit File for Tax Purposes) within VAT Groups.

- Treatment of eInvoicing reporting requirements.

Further clarification and technical specifications are expected in upcoming regulations or administrative instructions.

Impact for businesses

- VAT Groups allow for streamlined, consolidated reporting and potential administrative efficiencies.

- Individual entities must maintain separate compliance for regular VAT returns and payments.

- Businesses considering VAT Group formation should assess ownership structures, voting rights, and shared economic activity, while monitoring forthcoming guidance on SAF-T and eInvoicing integration.

Romania

Adoption of EU SME VAT scheme

Published: 28 August 2025 | Effective: 1 September 2025

Summary:

Romania has aligned its VAT legislation with Council Directive (EU) 2020/285 and Directive (EU) 2022/542, as well as Regulation (EU) No 904/2010, by adopting the special scheme for small enterprises (SME Scheme). This was implemented through Ordinance No. 22 of 28 August 2025.

The changes bring Romania in line with EU rules regarding:

- Special regime for small entities (SME Scheme)

- Place of provision of services, including virtual events

- VAT registration threshold

SME Scheme eligibility

A taxable person established in another EU Member State may apply the special exemption regime in Romania if the following conditions are met:

- EU-wide turnover: Does not exceed €100,000 in the current and previous calendar year.

- Romania-specific turnover: Does not exceed 395,000 leu in the current and previous calendar year.

Place of Provision Rules

- Physical events: Place of supply is where the event physically takes place.

- Virtual events: Place of supply is where the beneficiary is established, has a permanent address, or habitual residence.

VAT Registration Threshold

- Threshold: 395,000 leu per calendar year.

- Taxable persons exceeding this threshold must register for VAT in Romania.

Impact for Businesses

- Facilitates cross-border SME trade by allowing eligible EU businesses to benefit from VAT exemptions in Romania.

- Clarifies place of supply rules for physical and virtual services, aligning with EU VAT practices.

- Businesses must monitor turnover both at EU level and specifically within Romania to maintain eligibility for the SME scheme.

Slovenia

Simplified digital tool for VAT Ledger Reporting

Published: 13 October 2025 | Platform: FURS eDavki

Summary:

The Financial Administration of the Republic of Slovenia (FURS) has launched a user-friendly digital solution for submitting VAT Records of Sales and Purchases (VAT ledgers). The initiative introduces an Excel-based template that simplifies data preparation and submission, converting files automatically into CSV format compatible with the eDavki platform.

Key features of the digital tool

- Excel Template: Structured, transparent and easily readable format for VAT ledger reporting.

- Automatic CSV Conversion: Uploaded Excel files are converted into the required format for the eDavki portal.

- Validation: The system checks structural and logical accuracy and provides instant feedback for corrections.

- Support Resources:

- Technical documentation with detailed change logs.

- FAQ section updated on 15 October 2025 for guidance on VAT ledger obligations

Once completed, the Excel file can be uploaded directly to FUR’s platform where it is:

Scope and applicability

- Applies to all VAT-registered taxpayers, including non-established businesses in Slovenia.

- Supports testing and verification of VAT ledger data, especially for amended or corrected submissions.

- Serves as an educational tool for understanding proper VAT ledger completion.

Benefits for Taxpayers

- Simplifies VAT ledger preparation and submission.

- Ensures compliance through automated validation.

- Provides clarity and guidance with structured templates and comprehensive documentation.

- Supports Slovenia’s transition toward fully digital reporting practices.

Sweden

Invoice formal requirements and deduction for input tax

Published: 9 September 2025

Summary:

The Swedish Tax Agency has updated its VAT guidance on proving input VAT deduction to reflect the ECJ ruling in Case C-726/23 Acromet Towercranes. The ruling clarifies the conditions under which input VAT may be claimed, even if invoices do not meet all formal requirements.

Key points:

- Invoice Formalities: Input VAT deduction cannot be denied solely due to missing formal invoice elements.

- Material Conditions: The right to deduct remains valid if the substantive criteria for VAT deduction are met.

- Additional Documentation: Buyers may provide supplementary evidence beyond the invoice to prove that:

- The transaction occurred.

- The goods or services were used for taxable business activities.

- Proportionality: Any additional documentation requested must be limited and proportionate to what is necessary to support the deduction.

Implications for businesses

- VAT-registered businesses can claim input VAT even if invoices are incomplete, provided they can substantiate the business use of the transaction.

- Companies should retain supporting documentation (e.g. contracts, delivery notes) to demonstrate compliance with the deduction requirements.

- Reduces administrative burden by emphasizing substance over form for VAT deduction claims.

Bhutan

Registration threshold

Published: 18 June 2025 | Effective: 1 January 2026

Summary:

The National Assembly of Bhutan adopted the Goods and Services Tax (Amendment) Bill 2025, introducing a GST registration threshold for businesses operating in Bhutan.

Under the new law, businesses with an annual turnover exceeding BTN 5 million (approximately €48,600) will be required to register for GST.

The Bill has been transmitted to the National Council for further consideration and is scheduled to take effect from 1 January 2026.

Columbia

New reporting obligations for Digital Platform Operators introduced by DIAN

Published: 30 September 2025

Summary:

The Colombian Tax Authority (DIAN) has introduced new reporting obligations for Digital Platform Operators under Resolution 000227, in line with Law 1661 of 2013 and the Multilateral Competent Authority Agreement on the Automatic Exchange of Information on Income Derived through Digital Platforms.

Key updates:

- Reporting obligations apply to all Digital Platform Operators from the 2025 fiscal year

- Includes platforms providing:

- Services facilitated through platforms (transport, delivery, manual labor, tutoring, advertising, data processing, administrative, legal, accounting)

- Short- and long-term rentals of real estate

- Submission deadlines for the 2025 reporting year is 27 February 2026

- Annual reporting schedule applies to subsequent years

- Technical specifications and content requirements outlined by DIAN

Kazakhstan

New regulations announced around foreign online platforms

Published: 28 October 2025

Summary:

Kazakhstan has introduced new regulations affecting goods purchased by individuals from foreign online platforms, reclassifying them as “e-commerce goods” and establishing updated VAT and customs duties.Key updates:

Reclassification of goods

- Previously, goods purchased by individuals from foreign platforms were treated as personal goods.

- Under the new regulations, these are classified as e-commerce goods, subject to VAT and customs duties (details in the VAT rate changes section).

- The transition is expected to be smooth, with minimal disruption for parcel recipients.

Role of e-commerce operators

- Designated e-commerce operators (e.g., Kazpost JSC, DHL, FedEx) will handle:

- Customs declarations on behalf of recipients

- Processing and delivery of parcels

- Operators act as intermediaries to ensure compliance with customs and VAT requirements, while maintaining a similar logistics experience for consumers.

Customs duties and VAT

- New VAT and duty obligations will apply to imported e-commerce goods.

- The majority of consumers will experience little to no change in parcel receipt procedures due to the operator-handled clearance process.

- The rules aim to simplify customs clearance and ensure imported goods are taxed in line with international e-commerce standards.

Implications for businesses and consumers

- E-commerce operators must implement systems to submit declarations and calculate VAT/duties.

- Consumers should be aware that imported parcels may now include applicable VAT and customs duties.

- The new framework aligns Kazakhstan with global e-commerce taxation practices.

Switzerland

Federal Council advances VAT Digitalisation with Online Payment Method management

Published: 8 September 2025 | Effective: Immediate

Summary:

The Swiss Federal Council has introduced a new feature enabling taxpayers to select and manage their VAT payment methods online, marking a significant step in the digitalisation of Swiss VAT administration.

Key features:

- Taxpayers can now update preferred VAT payment methods directly through the official ePortal: https://www.mwstabrechnen.estv.admin.ch/pro/home

- Changes are immediately reflected in the taxpayer’s official records, eliminating the need for paper forms submitted by post.

Implications for businesses

- Simplifies the administrative process for updating payment methods.

- Enhances efficiency and accuracy of VAT compliance records.

- Aligns Switzerland with European digital reporting standards and promotes a more accessible VAT environment for businesses.

Benefits:

- Reduces paperwork and postal delays.

- Improves taxpayer experience through real-time updates.

- Supports ongoing efforts to modernise VAT compliance and facilitate digital reporting.

Switzerland

Online-only procedure for VAT Return extension Requests

Published: 1 September 2025 | Effective: Immediate

Summary:

The Swiss Federal Tax Administration (FTA) has announced that all requests for extensions to submit VAT returns must now be submitted exclusively via the official ePortal “VAT return” service.

Key updates:

- Electronic submission of extension requests is mandatory under Article 123 of the VAT Ordinance.

- Requests submitted by paper or other means will no longer be accepted or approved.

- This ensures that all extension requests are processed consistently and efficiently.

Implications for taxpayers:

- Taxpayers must register for and use the FTA ePortal to request deadline extensions.

- Streamlines communication with the FTA and reduces administrative delays.

- Supports Switzerland’s broader goal of fully digitalized VAT administration.

Benefits

- Ensures compliance with official procedures.

- Provides immediate confirmation of submission through the ePortal.

- Reinforces consistency and transparency in VAT reporting processes.

UAE

Updated Registration Forms and Criteria for VAT Tax Groups

Published: 13 October 2025 | Effective: Immediate

Summary:

The Federal Tax Authority (FTA) has updated the registration and amendment forms for VAT Tax Groups, which allow related entities under common management to consolidate VAT reporting as a single taxable person.

Key updates:

- A VAT Tax Group is treated as a single taxable person, with one Tax Identification Number (TIN) for all group members.

- A representative member must be appointed to submit a consolidated VAT return covering all sales and purchases of the group.

- The updated forms include:

- Eligibility clarification: Only entities established in the UAE may join a VAT Tax Group.

- Detailed turnover disclosure: Applicants must provide monthly sales turnover data, broken down by VAT rate, including exempt supplies, for the preceding 12 months.

- Supporting documentation: Forms must be signed, stamped, and accompanied by evidence of turnover, such as invoices, supply summaries, and contracts.

Implications for businesses

- Entities planning to form or join a VAT Tax Group must ensure all turnover and supporting documents are accurate and complete.

- Additional conditions for VAT Group formation include ownership structure, control relationships and shared economic activity among group members.

- Compliance with these requirements ensures streamlined VAT reporting and avoids potential FTA penalties.

Benefits

- Simplifies VAT compliance for multiple related entities.

- Reduces administrative burden by allowing consolidated reporting.

- Enhances transparency and accuracy in VAT filing.

United Kingdom

HMRC fully digitalises VAT return corrections

Published: 5 September 2025 | Effective: Immediate

Summary:

HMRC continues to streamline VAT compliance by fully transitioning to an online VAT correction process. The traditional VAT652 form has been fully phased out and will no longer be accepted, even by post.

Key features of the Online Correction Process

- Taxpayers and their agents can now correct VAT return errors online.

- Corrections may be made on the next VAT return if the net difference meets the following thresholds:

- £10,000 or less, or

- Between £10,000 and £50,000, provided it is less than 1% of total sales.

- Corrections exceeding these thresholds require:

- Amending the original reporting period, and

- Submitting a full explanation, including steps to prevent similar errors in the future.

Implications for businesses

- Non-compliance with the thresholds or reporting requirements may result in penalties.

- Businesses unable to submit corrections online must provide a detailed explanation with fully laid-out figures by post.

- This change is part of HMRC’s commitment to digital VAT processing, improving efficiency and reducing administrative burden.

Benefits

- Streamlines VAT error corrections and reduces the need for paper-based submissions.

- Enhances transparency in reporting and ensures timely resolution of VAT discrepancies

Work with indirect tax experts

Navigating global indirect tax doesn’t have to be complicated. At Fintua, our dedicated team brings clarity to compliance. Whether you’re expanding into new markets or streamlining existing obligations. We combine expert insight with tailored technology to support businesses in a digital-first landscape. Whatever the jurisdiction, whatever the challenge – we’re ready.

Subscribe to our newsletter

Stay informed about the latest VAT news, trends and topics from around the globe with our monthly newsletter. Each month, we deliver insightful updates straight to your inbox, helping you stay ahead of the curve.

Authors

Lisa Dowling

Specialising in International VAT Compliance solutions, Lisa brings a wealth of knowledge and insight in her dealings with a host of international clients ranging from start-ups through to multinationals. With 21 years VAT experience behind her, Lisa has managed VAT compliance issues and solutions globally for over 11 years. Fintua have 12,000 + corporate clients in over 109 countries and many of these are members of the Fortune 500.